The past decade brought a rise in sugar-related discussions amongst the food and beverage industry, public health officials and the general population. While demand for sugar and sweeteners has never been higher, the need for sugar reduction has also continued to grow. Sugar, in the form of the carbohydrate glucose, is the primary energy of life. It is the main source for the human body, as all carbohydrates are broken down into sugars by our body to perform. For instance, the human brain needs around 50 grams of sugar per day to function.

This is one of the reasons humans evolved to find the taste of sugar favourable; it is something we need, so a strong liking of the taste drives consumption of foods containing sugar that would help fuel our body. This was especially important during human evolution when sources of sugar were not as easily accessible as they are now. However, there is a difference between naturally occurring / free sugars and added sugars. How do consumers tell the difference?

The WHO definition of term free sugars refers to ‘monosaccharides (such as glucose, fructose) and disaccharides (such as sucrose or table sugar) added to foods and drinks by the manufacturer, cook or consumer, and sugars naturally present in honey, syrups, fruit juices and fruit juice concentrates’. By this definition, for example, fruit juice would contain free sugars but might not be considered an ‘added sugar’ unless it was added to another food or beverage for the purpose of sweetening. The EFSA and FDA go into further detail about definitions of what is and isn’t an added sugar. Added sugars are considered empty calories (i.e. supplying energy but little else nutritionally) and therefore have been the focus of increasing attention in dietary guidelines in recent years.

As per European Regulation (EU) No 1169/2011 on the provision of food information to consumers “sugars” are defined as “all monosaccharides and disaccharides present in food, but excludes polyols”. To date, there is no similar clear-cut definition of the term ‘added sugars’ in the same piece of Regulation. However, Regulation (EC) No 1924/2006 on nutrition and health claims made on foods does reference a “No Added Sugar” claim as “where the product does not contain any added mono- or disaccharides or any other food used for its sweetening properties.” Within the food industry, this then prompts discussion on how to define “any other food used for its sweetening properties”.

In the United States, the FDA definition of added sugars includes sugars that are either added during the processing of foods, or are packaged as such, and include sugars (free, mono- and disaccharides), sugars from syrups and honey, and sugars from concentrated fruit or vegetable juices that are in excess of what would be expected from the same volume of 100 percent fruit or vegetable juice of the same type. The definition excludes fruit or vegetable juice concentrated from 100 percent fruit juice that is sold to consumers (e.g. frozen 100 percent fruit juice concentrate) as well as some sugars found in fruit and vegetable juices, jellies, jams, preserves, and fruit spreads.

It is the consumption of increased added sugars that is blamed for various health conditions such as increase of a person’s risk for heart disease, type two diabetes, and obesity. Additionally, there is a strong link between sugar intake and dental caries, or more commonly known as tooth decay or cavities. It has been estimated that, globally in 2010, US$ 298 billion was spent on direct costs associated with dental caries (WHO).

It’s no surprise the focus from the authorities around sugar reduction. Reducing sugar consumption is a global focus as a health imperative, the World Health Organization recommends reducing free sugar intake for both children and adults to under 10 percent of total daily calories, equivalent to around 50 grams of free/added sugar maximum for the average person per day. It is undeniable that overconsumption of sugars – added sugars – has been recognized as a worldwide problem by top public health agencies and consumers’ interest regarding reducing sugar consumption over time is maintained high.

In addition to the health benefits, that reducing sugar consumption can also be linked to sustainability improvements.? Sugar production can have an adverse impact on the environment in many ways, so reducing consumption can also promote sustainability.

Environmental Impact of Sugar Production

Sugar is a major industry with significant effects on the global environment resulting from growing, harvesting, refining, and distribution. On average, sugarcane accounts for nearly 80% of global sugar production, with some 110 countries currently producing sugar from either cane or beets. For the period October/ September 2019, the top 10 producing countries (India, Brazil, Thailand, China, the US, Mexico, Russia, Pakistan, France, and Australia) accounted for nearly 70% of global output, with more than 170 million tonnes consumed annually (International Sugar Organisation). The production of sugar is a highly water intensive operation, especially from sugar cane which has deep roots.

According to a recent sugar life cycle analysis and report conducted by Kerry, manufacturing 1kg of cane sugar uses 1,110 liters of water and leads to 0.42kg of CO2 emissions. For the case of beet sugar, it would require 640 liters of water and emit 0.85kg of CO2e (LCA).

The increase in global demand for sugar is resulting in highin high water consumption, air and water pollution, soil degradation, and change in natural habitat. It is estimated that 10% of soil is lost during harvest of beet sugar and 3-5% of soil in sugar cane harvest. This has resulted in the clearing of natural habitats such as rain forests, coastal wetlands, and savannah (WWF Action for Sustainable Sugar).

|

Get KHNI articles delivered to your inbox

|

Global Sugar Reduction Initiatives

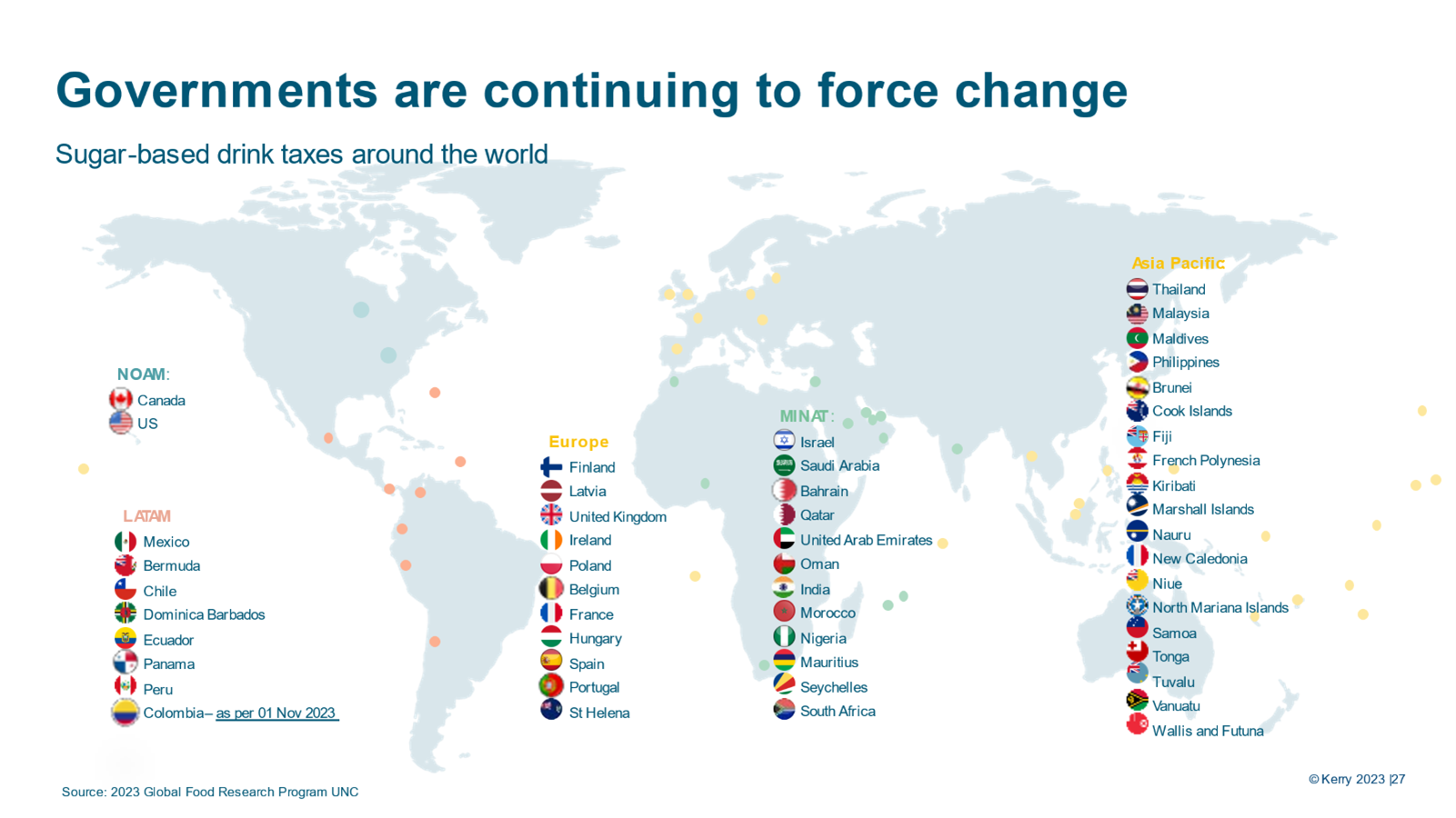

Following the 2015 publication of the World Health Organization’s “Global Action Plan for the Prevention and Control of Noncommunicable Diseases 2013–2020” (GAP), 20 governmental bodies introduced taxation intended to reduce obesity and rising levels of diabetes, most often by targeting sugar sweetened beverages (SSBs) as they have been determined to be a major source of added/ free sugars. By mid-2018, 39 countries, states and cities had introduced nutritional taxation with more working toward voluntary sugar reduction approaches to encourage optimised nutrition.

Today, that number continues to grow, with more than 50 countries or jurisdictions having implemented taxes on sugary drinks as a way to discourage consumption. Among the latest places to turn to taxation as a means of encouraging healthy habits and fighting obesity-related illness are Spain and Poland, which introduced new sugar taxes in January of 2021.

In the same time, there are front-of-pack labelling initiatives that are implemented across the countries on a global level. Those initiatives seem to attract even more consumer’s attention. They are easier to be interpreted by the consumer and have alerted manufacturers since they have an impact on the marketing of a products as they may restrict the advertisement of unhealthy foods.

- Although sugar taxes have been a developed world reality, some of the earliest and most enthusiastic adopters are emerging markets. According to the PLoSONE journal article “Regulatory initiatives to reduce sugar-sweetened beverages (SSBs) in Latin America”, 14 Latin American countries have adopted public and private SSB initiatives since 2006. These include Mexico, which has one of the highest rates of diabetes globally, and Chile which coupled its tax with warning labels on foods high in sugar, fat or sodium.

- Hungary was another early adopter, with the introduction of its broad “health tax” in 2011 which took aim at a range of products including those containing high fat and sodium. Today, around a dozen European countries have some form of sugar or health tax, including the UK, Ireland, France and Portugal.

- In the North America, Canada introduced a front-of-pack nutrition symbol in 2023 that is required on foods high in sugar, sodium and/or saturated fat. United States does not currently have a national strategy for SSB taxation, although city authorities such as those in Berkeley, California, and Boulder, Colorado, have introduced local measures.

- Among nations in the Middle East and Africa, sugar taxes are in play in countries including Saudi Arabia, the United Arab Emirates, Oman, Morocco, Nigeria and South Africa. In Asia Pacific, several long-standing sugar taxes are in effect and more recent legislation has been applied in Thailand, Philippines and Malaysia.

The structure of the taxes often follows a similar pattern, usually with a tiered system that awards a higher tax for products with higher sugars. In most cases the tax is passed on to the final consumer, though some manufacturers have managed to mask price increases through the introduction of smaller pack sizes.

In addition to applying pressure to cost-conscious consumers, sugar taxes incentivise manufacturers to rethink recipes and create nutritionally optimised food and beverages.

For example, ahead of the introduction of the UK Soft Drink Industry Level (SDIL) sugar tax in April of 2018, manufacturers began reformulating products, shrinking the number of high- and mid-sugar soft drinks in their portfolio and increasing their low- and zero-sugar offerings. A study in BMC Medicine found that 6 of the top ten brands affected by the SDIL reformulated more than half of the products in their portfolios between 2015 and end of 2018. As these products hit the market, the total volume sales of high- and mid-sugar soft drinks was cut in half, while volume sales of low- and zero-sugar drinks rose by 40%. A separate report on the SDIL found that around its implementation, sugar content in soft drinks was reduced by an average of 44%.

A similar pattern can be seen across Latin America, where 15% of the carbonated soft drinks launched in 2023 had a reduced/low/no or free sugar claim, reflecting the current focus of both the industry and the consumer. In Brazil, the food and beverage industry agreed to voluntarily reduce sugar in over 1,100 products by 2022. Some participating manufacturers have also made voluntary commitments to the reduction of sodium, suggesting that overall nutrition optimisation is an increasingly popular goal. New labeling requirements, including in Mexico the Official Mexican Standard NOM-051-SCFI/SSA1-2010 and Brazil the NORMATIVE INSTRUCTION-IN NO. 75, OF OCTOBER 8, 2020 – NORMATIVE INSTRUCTION-IN NO. 75, OF OCTOBER 8, 2020 – DOU – Imprensa Nacional, are also pressuring brands to create lower sugar products.

Even in markets and categories without formal legislation, there is still considerable pressure on manufacturers. In the United States, The National Salt and Sugar Reduction Initiative (NSSRI) is in the process of setting voluntary sugar reduction targets after having gotten widespread commercial support for its salt reduction infrastructure.

In the UK, some SSBs that fall outside of the SDIL purview, including unsweetened juices and sweetened milk-based beverages, have seen sugar reductions of around 10% following requests from Public Health England. (Other products have fared worse, leading many to call the voluntary initiative a failure.) Germany, voluntary targets have been set and, although no official taxes have been introduced, a small consumer survey suggests such efforts would have popular approval.

As low sugar, no added sugar, reduced and free sugar claims become more prominent in new product launches, reformulation efforts are improving and consumer perceptions about reduced sugar beverages—which have historically faced taste and texture challenges—are changing.

Consumers Attitudes Toward Different Sweeteners

Striking the balance between taste and nutrition is now more crucial than ever before. People are not demanding but expecting food and drink that provide them with accessible and nutritional solutions that also cater to their taste buds.

The need for sugar reduction is undeniable – 79%1 of global consumers believe that reduced sugar food and drinks are healthier than full sugar versions. Consumer’s sweetness expectations are no longer nebulous. They are voicing their sugar reduction desires and laying down rules. The degree of ‘desired’ sugar reduction is complex.

What sweetener? In what product? Natural or artificial? And how much?

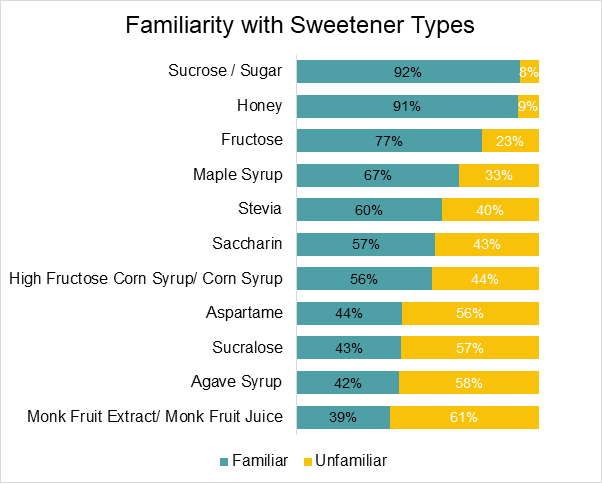

The type of sweetener used in food and drink is important to 77%1 of consumers globally. There’s lots of variables in the reduced sugar conversation, and consumers’ preferences vary considerably depending on the food or drink in question. The figure below shows consumer familiarity when it comes to different types of sweeteners:

This understanding is important to consider when we look at which sweeteners consumers would prefer. In the table below, honey was the most preferred sweetener among all consumers, followed by sucrose. Neotame, advantame were the least preferred (do not prefer).

Preference for Sweeteners (% – Global; Base = Total Respondents)

Although taste remains a primary driver of sugar consumption, consumers increasingly acknowledge and turn to reduced sugar products as healthier alternatives.

Eighty-one percent of global consumers indicate diabetes and weight gain as significant drawbacks of sugar consumption, which are major deterrents. Hence, the need for sugar reduction is undeniable, with 79% of global consumers believe that reduced sugar food and drinks are healthier than full sugar versions. (© Kerry Proprietary Consumer Research | Sensibly Sweet 2023 | n=12.784)

In a World That Loves Sugar’s Familiar Qualities…Where to Start for Successful Reduction?

The responsibility and cost of helping consumers reduce their sugar intake is being pushed onto the food and beverage industry. Why so many sugar-reduced products fail? Though consumers cite taste as the biggest driver of their intention to repurchase, what are the other key factors that may stop great-tasting products from getting off the shelf.

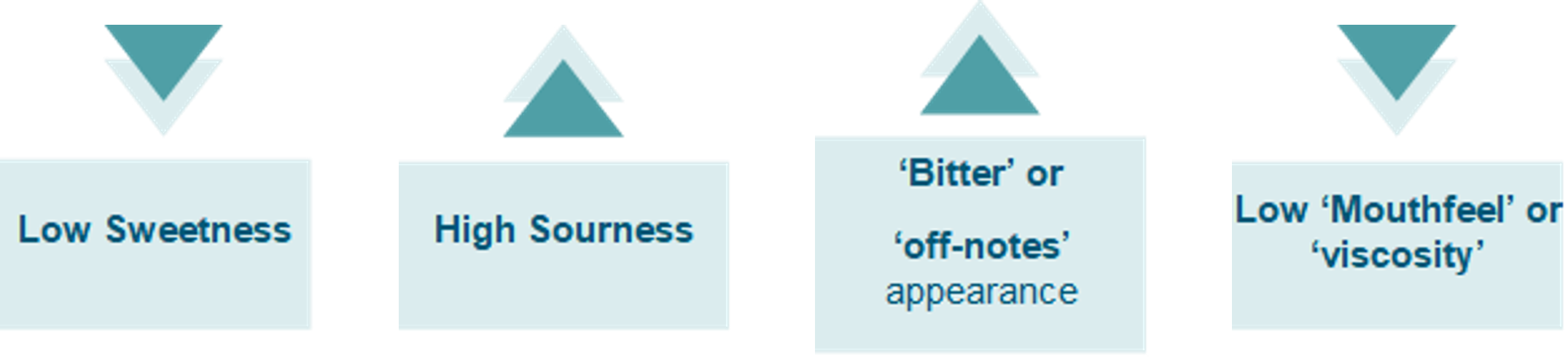

Every product category has different challenges when reformulating or developing from a low/no sugar added base. From Beverages to dairy, from bakery to sauces the approach is different. Reducing sugar or developing from a low/no sugar base in beverages needs to address simultaneously various challenges; low overall sweetness, high sourness, appearance of bitterness and off-notes while product mouthfeel is low.

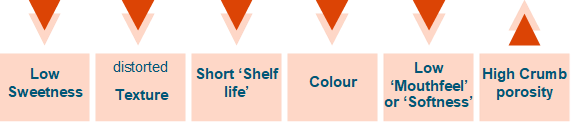

Considering the bakery product category the challenges are different to beverages; sweetness and mouthfeel are low, however now parameters as texture, shelf life, colour and crumb porosity are also impacted.

There is not one solution fits all. The approach is usually a combination of various ingredients that work in synergy to address the various challenges. From the selection of the desired sweetening system, to texturants and preservation systems the choices are dependent to your formulation and target consumer. However, as taste is the primary driver when it comes to consumer’s purchase behaviour, flavours have a significant role to play in the formulation of reduced and low/no sugar containing products. Flavours with modifying properties, mouthfeel and masking are used to optimize the sweetness profile of the product, deliver clean sweet taste and offer full-bodied mouthfeel with no off notes while optimizing the flavor profile when sugar is being reduced/ low or not present in the product formulation. They work in synergy with the rest of the ingredients present in food & beverages enabling great clean taste without off notes that consumers will crave for.

The sugar market has been greatly challenged the last years, with global deficit in the 2021/22 season replaced by a global surplus in 2022/23 season. This crop uncertainty has a high impact on the whole supply chain of sugar. Sugar is universally used across food and beverages industry. Hence there is a major need for cost stabilization and potentially savings in the various product offerings to address consumer need for affordable nutrition in the current volatile environment.

Conclusion

Although there has been significant progress in sugar reduction and sweetness optimisation technology, there is still some way to go. The sugar consumption is increasing in the years. Diabetes, obesity and teeth decay are still high in the health agenda’s agendas globally. Therefore, there is still much to play for as manufacturers stride to offer great tasting products that meet lower sugar targets and do not impact taste, texture and shelf life.